- Equity Research Cheat Sheets

- Posts

- UURAF - 2Q Review - Refresher before Q3 EPS results. Bull case $14.50 Bear case $1.50

UURAF - 2Q Review - Refresher before Q3 EPS results. Bull case $14.50 Bear case $1.50

Cheat Sheets

UCORE RARE METALS (UURAF)

📊 Q2 Loss -$3.63M CAD (Improved 29% QoQ) | $22.4M DoD Funding Secured | RapidSX™ Tech Validated | Louisiana Facility Groundbreaking | China Export Controls = Opportunity

Pre-Revenue Development Company | Heavy Rare Earth Processing Focus | Commercial Production Target H2-2026 | Strategic US Government Partnership | North American Supply Chain Independence | Patent-Pending Separation Technology

💰 Market Cap: $479M | 🏢 170 Employees | 🌍 Canada/USA Operations

👨💼 CEO Pat Ryan | 🎯 Rare Earth Independence | 🇺🇸 Louisiana/Alaska/Ontario

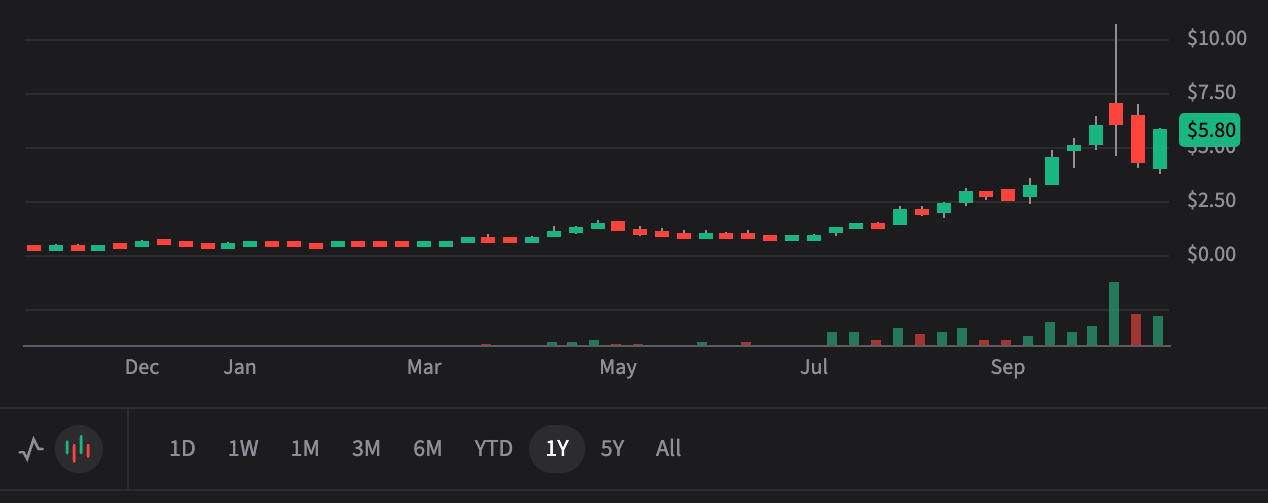

$5.25

📈 +$0.30 (+6.1%) Today

+1,130% YTD | Down -51% from Oct High

Price Targets (12-18 Months)

Current Price: $5.25 USD

$14.50

Bull Case (+176%)

2027 Revenue: $45M Est | EV/Revenue: 10x

COMMERCIAL SUCCESS

🚀 Needs:

Louisiana SMC achieves 2,000 tonne TREO annual capacity by Q4-2026 • RapidSX™ patent granted and technology licensing deals secured • Multiple offtake agreements with Western manufacturers signed • China maintains export restrictions driving demand for independent supply • DoD awards additional Phase 3 funding for capacity expansion • Bokan Mountain project advances with positive feasibility study

$8.50

Base Case (+62%)

2027 Revenue: $25M Est | EV/Revenue: 8x

MEASURED EXECUTION

⚖️ Needs:

Louisiana SMC begins early production H2-2026 with initial 500-800 tonne capacity • RapidSX™ technology proves commercially viable at full scale • Secures feedstock supply agreements with 2-3 upstream partners • Maintains DoD relationship with continued project milestones • Raises additional $30-50M capital at reasonable dilution for Phase 1 completion • Demonstrates cost-competitive separation vs. Chinese processors

$1.50

Bear Case (-71%)

2027 Revenue: Delayed | Book Value Multiple

EXECUTION FAILURE

⚠️ Risk:

RapidSX™ patent application rejected and technology copied by competitors • Louisiana SMC construction delays push commercial production to 2028+ • Unable to secure cost-competitive feedstock amid Chinese market dominance • Requires significant additional capital raises at <$2.00 causing massive dilution • China relaxes export restrictions flooding market with cheap REEs • DoD shifts priorities away from rare earth processing support • Technology fails to scale commercially from demonstration to production levels

The TL;DR

💰

What Happened

Q2 Net Loss: -$3.63M CAD improved 29% from Q1's -$5.12M CAD loss

DoD Funding: Secured $18.4M Phase 2 award bringing total to $22.4M for commercial-scale RapidSX™ machine

Facility Progress: Louisiana SMC groundbreaking completed May 29, 2025 at 80,800 sq ft England Airpark location

Tech Validation: Successfully separated critical HREEs terbium and dysprosium in Phase 1 demonstration

Capital Raise: Closed C$15.5M brokered offering in June 2025 to fund commercial operations

DoD Funding: Secured $18.4M Phase 2 award bringing total to $22.4M for commercial-scale RapidSX™ machine

Facility Progress: Louisiana SMC groundbreaking completed May 29, 2025 at 80,800 sq ft England Airpark location

Tech Validation: Successfully separated critical HREEs terbium and dysprosium in Phase 1 demonstration

Capital Raise: Closed C$15.5M brokered offering in June 2025 to fund commercial operations

📈

Why It Matters

Strategic Timing: China's Oct 2025 rare earth export restrictions validate Ucore's North American supply chain strategy

Government Backing: Non-repayable DoD funding de-risks commercial scale-up with US national security priorities

Market Monopoly: China controls 90%+ of global rare earth processing; Ucore targets critical supply gap

Tech Moat: RapidSX™ patent-pending technology offers faster, cleaner separation than conventional methods

Defense Demand: National Defense Authorization Act bans Chinese REE imports for defense sector effective Jan 2027

Government Backing: Non-repayable DoD funding de-risks commercial scale-up with US national security priorities

Market Monopoly: China controls 90%+ of global rare earth processing; Ucore targets critical supply gap

Tech Moat: RapidSX™ patent-pending technology offers faster, cleaner separation than conventional methods

Defense Demand: National Defense Authorization Act bans Chinese REE imports for defense sector effective Jan 2027

🎯

What's Next

Q4-2025: Complete commercial-scale RapidSX™ machine construction and begin commissioning activities

H2-2026: Achieve "Early Production" of salable rare earth oxides from Louisiana SMC facility

2026-2027: Scale to 2,000 tonne TREO annual capacity with modular RapidSX™ unit additions

Supply Chain: Execute binding offtake agreements with Western manufacturers and secure feedstock partnerships

Expansion: Advance Bokan Mountain Alaska project and pursue additional SMC locations in Canada

H2-2026: Achieve "Early Production" of salable rare earth oxides from Louisiana SMC facility

2026-2027: Scale to 2,000 tonne TREO annual capacity with modular RapidSX™ unit additions

Supply Chain: Execute binding offtake agreements with Western manufacturers and secure feedstock partnerships

Expansion: Advance Bokan Mountain Alaska project and pursue additional SMC locations in Canada

💡

Bottom Line for Retail Investors

Ucore is a high-risk, high-reward play on North American rare earth supply chain independence. The company has validated its RapidSX™ technology at demonstration scale and secured critical $22.4M DoD funding to build the first commercial facility in Louisiana. With China tightening export controls on the very elements Ucore will produce (dysprosium, terbium, neodymium, praseodymium), geopolitical winds are strongly favorable. However, execution risk is massive—this is a pre-revenue company that must successfully scale unproven technology, secure feedstock, and reach commercial production by late 2026. The 1,130% YTD stock run reflects both the strategic opportunity and speculative nature. Perfect for investors who understand this is essentially a leveraged bet on US rare earth independence, with DoD backing as the ultimate risk-reducer. Not for the faint of heart, but the strategic positioning is undeniable as Western nations scramble to break China's rare earth monopoly.

🐂 Bull Thesis

🇺🇸

Strategic National Priority

DoD Partnership: $22.4M non-repayable funding validates strategic importance and de-risks execution

Defense Mandate: Jan 2027 ban on Chinese REEs for defense sector creates guaranteed domestic demand

China Risk: Oct 2025 export controls on dysprosium, terbium create immediate supply urgency for Western manufacturers

Bipartisan Support: Rare earth independence has Republican and Democratic backing as critical national security issue

Defense Mandate: Jan 2027 ban on Chinese REEs for defense sector creates guaranteed domestic demand

China Risk: Oct 2025 export controls on dysprosium, terbium create immediate supply urgency for Western manufacturers

Bipartisan Support: Rare earth independence has Republican and Democratic backing as critical national security issue

⚗️

Proven Technology Moat

Demonstration Success: 2,600+ hours operation, 3+ tonnes processed, high-purity outputs achieved at Kingston facility

Patent Pending: RapidSX™ proprietary solvent extraction offers faster processing and lower environmental impact vs traditional methods

Critical Elements: Successfully separated dysprosium and terbium—the hardest and most valuable heavy REEs

Modular Design: Scalable technology platform allows incremental capacity additions and capital-efficient growth

Patent Pending: RapidSX™ proprietary solvent extraction offers faster processing and lower environmental impact vs traditional methods

Critical Elements: Successfully separated dysprosium and terbium—the hardest and most valuable heavy REEs

Modular Design: Scalable technology platform allows incremental capacity additions and capital-efficient growth

🏭

Infrastructure in Place

Louisiana SMC: 80,800 sq ft facility secured at England Airpark with long-term lease and $15M+ state incentives

Tax Benefits: $8.2M in ad valorem tax savings over 10 years plus Foreign Trade Zone duty advantages

Construction Started: Groundbreaking completed May 2025, commercial-scale machine construction underway

Target Timeline: Early production H2-2026 with path to 2,000 tonne annual TREO capacity

Tax Benefits: $8.2M in ad valorem tax savings over 10 years plus Foreign Trade Zone duty advantages

Construction Started: Groundbreaking completed May 2025, commercial-scale machine construction underway

Target Timeline: Early production H2-2026 with path to 2,000 tonne annual TREO capacity

💎

Market Monopoly Opportunity

Supply Gap: China processes 90%+ of global REEs; Western capacity virtually non-existent for heavy REEs

Growing Demand: EVs, wind turbines, defense systems driving 5-7% annual REE demand growth through 2030

Premium Pricing: Strategic buyers willing to pay 10-30% premium for non-Chinese supply chain security

First Mover: Among first Western companies to achieve commercial-scale heavy REE processing capability in decades

Growing Demand: EVs, wind turbines, defense systems driving 5-7% annual REE demand growth through 2030

Premium Pricing: Strategic buyers willing to pay 10-30% premium for non-Chinese supply chain security

First Mover: Among first Western companies to achieve commercial-scale heavy REE processing capability in decades

🐻 Bear Thesis

🔬

Unproven Commercial Scale

Demonstration ≠ Production: Only 3 tonnes processed at demo scale vs. 2,000 tonnes annual target—massive scaling risk

Patent Pending: RapidSX™ IP not yet secured; competitors or China could replicate technology

No Revenue History: Zero commercial production track record; relies entirely on DoD grant funding currently

Technical Unknowns: Commercial-scale separation may reveal unforeseen challenges with cost, efficiency, or purity levels

Patent Pending: RapidSX™ IP not yet secured; competitors or China could replicate technology

No Revenue History: Zero commercial production track record; relies entirely on DoD grant funding currently

Technical Unknowns: Commercial-scale separation may reveal unforeseen challenges with cost, efficiency, or purity levels

💸

Massive Capital Requirements

Ongoing Losses: -$7.2M CAD burn in first half 2025 with no revenue until late 2026 at earliest

Funding Gap: DoD covers only portion of costs; needs $50-100M+ additional capital to reach commercial production

Dilution Risk: Stock up 1,130% YTD but down 51% from Oct high—future raises likely at distressed prices

Market Cap Disconnect: $479M valuation for pre-revenue company with unproven tech creates significant downside risk

Funding Gap: DoD covers only portion of costs; needs $50-100M+ additional capital to reach commercial production

Dilution Risk: Stock up 1,130% YTD but down 51% from Oct high—future raises likely at distressed prices

Market Cap Disconnect: $479M valuation for pre-revenue company with unproven tech creates significant downside risk

🇨🇳

Chinese Competition Threat

Cost Advantage: Chinese processors have 30-50% lower costs from scale, infrastructure, and looser environmental standards

Export Control Reversal: China could ease restrictions to maintain market dominance and undercut Western competition

Feedstock Control: China dominates upstream mining; securing consistent, cost-effective feedstock supply unproven for Ucore

Political Risk: Future US-China trade agreements could reduce strategic imperative for domestic processing

Export Control Reversal: China could ease restrictions to maintain market dominance and undercut Western competition

Feedstock Control: China dominates upstream mining; securing consistent, cost-effective feedstock supply unproven for Ucore

Political Risk: Future US-China trade agreements could reduce strategic imperative for domestic processing

⏰

Execution Timeline Risk

Aggressive Schedule: H2-2026 production target leaves minimal buffer for construction delays or technical issues

Permit Complexity: Environmental and operational permits for rare earth processing notoriously difficult and time-consuming

Supply Chain Dependencies: Requires coordinating multiple partners for feedstock, equipment, offtake simultaneously

Management Track Record: Team has demonstration success but no commercial production experience at this scale

Permit Complexity: Environmental and operational permits for rare earth processing notoriously difficult and time-consuming

Supply Chain Dependencies: Requires coordinating multiple partners for feedstock, equipment, offtake simultaneously

Management Track Record: Team has demonstration success but no commercial production experience at this scale

This analysis is for informational purposes only and should not be considered investment advice. Please consult with a financial advisor before making investment decisions. Ucore Rare Metals is a pre-revenue, development-stage company with significant execution and technology risks.